It is over a year now since the opening of the new, expanded locks at the Panama Canal. The new locks have had a significant impact on a number of areas of shipping, including the gas carrier sector, but the main focus of the project in Panama was always the container trade, and the Asia-US East Coast route in particular. In that regard, how do things look a little over one year on?

The new locks at the Panama Canal opened for transit on 26th June 2016, and the impact on the box shipping sector has been largely in line with expectations. The key area of impact was always going to be the Transpacific trade, and the Asia-US East Coast route in particular, the largest volume trade through the canal.

")

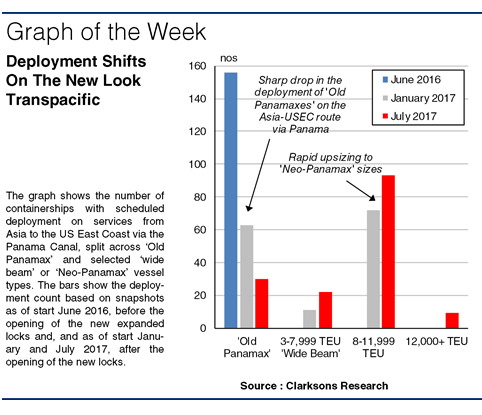

Following the opening, the Asia-USEC route immediately saw swift upsizing of ‘Old Panamax’ containerships, being replaced by ‘Neo-Panamax’ units, with operators aiming to benefit from the economies of scale offered by running larger vessels through the canal. Regular deployment of ‘Old Panamaxes’ on the Asia-USEC route via the canal has fallen from 156 units in June 2016 to 30 today.

The total of ‘old Panamaxes’ on the broader Transpacific trade now stands at 76, including some still operated via Suez to the USEC and from Asia to the USWC. However, there are around 35 ‘Old Panamaxes’ idle, and in total (based on a wide definition of 3,000+ TEU and ‘Old Panama’ beam) 101 have been scrapped since start 2016. Having said all that, there are still many of these units deployed elsewhere, with, on the same definition, over 450 outside the Transpacific.

")

Looking upwards, the initial impact last summer was a speedy upsizing of tonnage to ‘Neo-Panamaxes’. This, as expected, basically jumped the class of sub-8,000 TEU ‘wide beam’ ships; just 22 of those serve Asia-USEC today. Instead it focussed immediately on the 8-11,999 TEU ships, and today there are 93 of those deployed on the Asia-USEC. And now even units as large as 12,000+ TEU are getting in on the act, with 9 deployed Asia-USEC, taking total deployment of new ‘wider beam’ units there to 124.

This is all against a backdrop of robust growth on the Transpacific, with peak leg eastbound trade up by 8% y-o-y in Jan-May 2017. However, there hasn’t been any early sign of ‘cargo switching’ with flows proving ‘sticky’, even if USEC infrastructure constraints are diminishing (lifts at the 5 leading USEC ports as a share of lifts at the 5 major USWC ports is steady at c.80%). And interestingly the additional capacity on the Asia-USEC trade from the surge in upsizing has eroded the average Asia-USEC/Asia-USWC spot box freight rate ‘premium’ only gently, from 94% in 1H 2016 to 76% in 1H 2017.

So, plenty of questions remain. Will the Panamaxes finally fully depart the trade? Will a ‘cargo switch’ eventually evolve? How will the freight market trend? One year may have passed but it appears more time is needed to assess in full the longer-term impact of the new Panama locks on box shipping.

(Source : Clarksons)")