")

After reporting on a range of gloomy statistics in 2016, has shipping been able to pick itself up from ‘rock bottom’? Strong trade volumes, a record S&P market and improving bulker and containership markets have all provided some welcome relief. But challenges in the tanker, gas and offshore markets continue while uncertainty around environmental regulation builds. As ever, it’s been an interesting year!

ClarkSea Pick Up…

ClarkSea Pick Up…

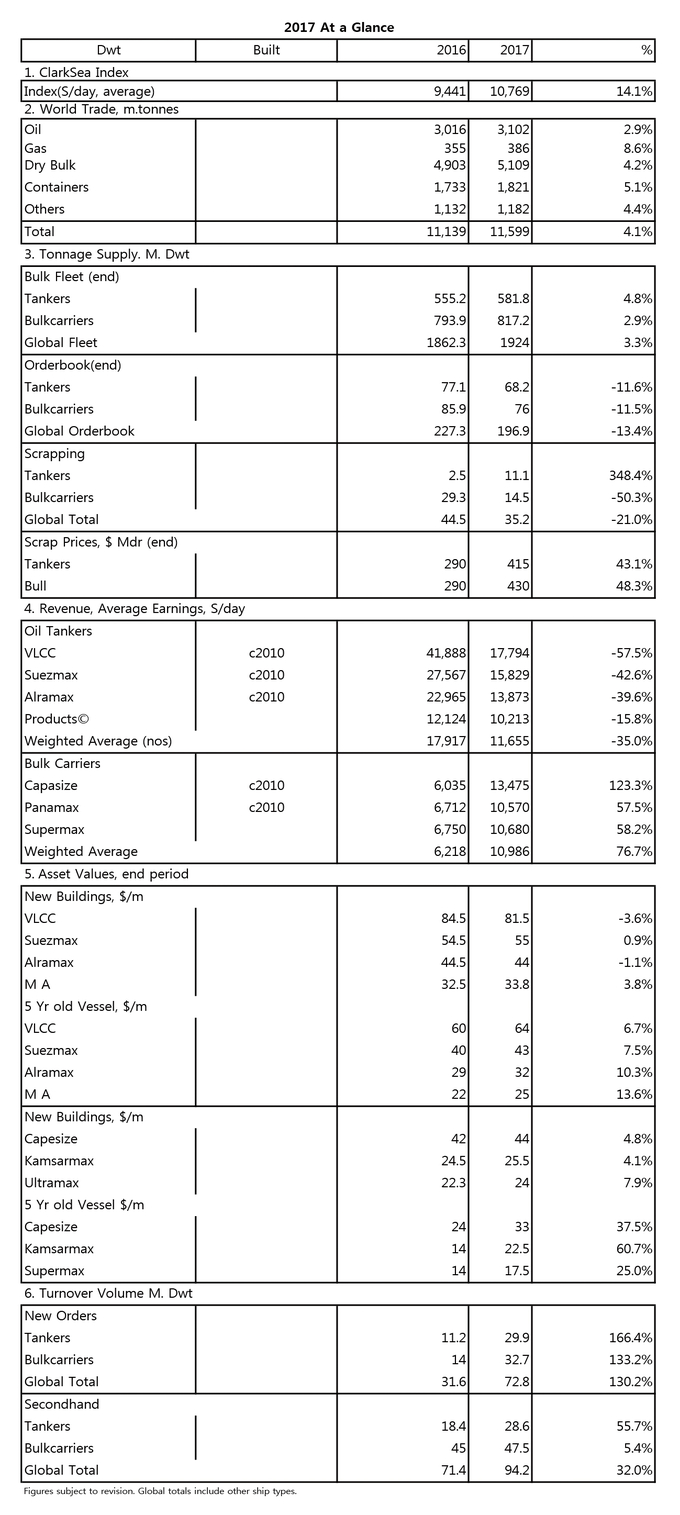

After its all time low in 2016, the ClarkSea Index, our indicator of vessel earnings, rose by 14% y-o-y to average $10,768/day. Some welcome relief but still 10% below the trend since the financial crisis and compared to OPEX of $6,394/day for the same basket of ships. It was also a year of contrasting fortunes across markets, especially ‘wet’ and ‘dry’.

Different Trajectories…

With overall earnings down 35%, the tanker market continued its ‘wind down’, struggling to absorb 5% fleet growth despite good developments in long-haul trades out of the Atlantic. Supportive fundamentals did flow through into an improving bulker market, with good first and fourth quarters helping rates jump by an impressive 77% y-o-y. The containership market seems to have picked itself up from the ‘shock’ of Hanjin’s collapse, with consolidation, improved but volatile freight rates and increasing charter rates and S&P prices (see next week for more detail). The gas markets have had to ‘tough it out’ but perhaps there is some ‘light at the end of the tunnel’, especially for LNG where trade grew by an encouraging 11% in 2017. The cruise and ferry markets had ‘solid’ years but the car carrier market had to wait until the end of the year for only marginal improvements. In offshore, increased FID and rig tendering and an improved oil price have been helpful but deep challenges remain. Offshore owners in a position to do so have been eyeing consolidation opportunities, especially in the rig sector, and S&P ‘bargains’. Overall some mixed trajectories but on balance encouraging signs.

Trade Surging…

After a sluggish few years, an improving world economy helped global seaborne trade to bounce back strongly in 2017, growing by 4.1% to 11.6bn tonnes, the fastest rate of growth since 2012. Demolition fell back to 35m dwt (tankers up 348% and bulkers down 50%) but trade still outpaced fleet growth (3.3%).

")

An S&P Record…

In our review of 2016, we reported it was ‘buy, buy, buy’ in the bulker market and during 2017 investors also placed containerships and tankers in their sights. In overall tonnage terms, 94m dwt represents an all time record, with boxships joining bulkers at record levels. Bulker S&P prices made excellent gains (a 5 year old Capesize up 38%), as did containerships but tanker gains were more modest. Greeks again topped the buyer (and seller) charts, followed by the Chinese (although German owners were the biggest sellers of containerships). Scrap prices moved up by over 40% to north of $400/ldt for the first time since 2013.

Watching The Yards…

After the 30 year ordering low of 2016, orders increased to 73m dwt in 2017, significant but still 24% below the average since the financial crisis. China returned to the top of the output charts, with a 39% share of deliveries, followed by Korea (32%) and Japan (21%). Delivery volumes were steady, although we expect them to decrease this year, while the overall orderbook declined 13% to 197m dwt of $233bn. As ever, it’s been an interesting year.

(Source : Clarksons)")