Chinese imports have swelled massively since China joined the World Trade Organization in late 2001, helping to propel global trade expansion. Chinese seaborne imports totalled 2.1bn tonnes in 2015, accounting for 20% of global imports, up from just 5% in 2001. However, Chinese economic growth eased in 2015, and expansion in imports slowed further, intensifying concerns over the future outlook.

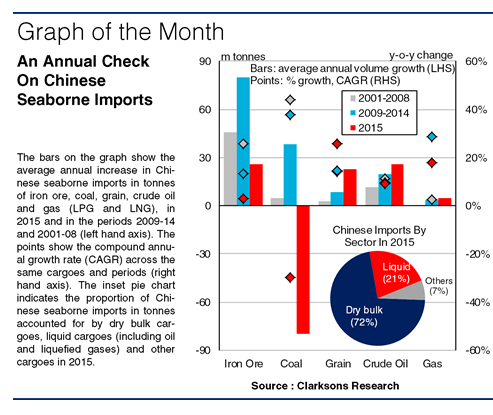

Between 2001 and 2008 Chinese seaborne imports grew by a CAGR of 17% p.a., to reach 1bn tonnes in 2008. This rapid growth was driven by an insatiable appetite for raw materials, as a result of booming construction and manufacturing activity. Even when the global financial crisis hit in 2008, China’s economic stimulus package helped imports to continue to grow strongly, and in 2009-14 imports expanded by a CAGR of 13% p.a. However, the rate of expansion in Chinese seaborne imports has seen a slowing trend in recent years, and imports grew by just 1% y-o-y in 2015.

The slowdown in import growth last year was largely due to a reduced appetite for dry bulk commodities, partly reflecting the continued shift in the economy away from a focus on heavy industry. Seaborne iron ore imports (which account for over 60% of China’s dry bulk imports) grew by just 3% y-o-y in 2015 to stand at 940mt, compared to a CAGR of 13% p.a. in 2009-14, reflecting declining domestic steel consumption and production, and closures of a number of steel mills.

Chinese coal imports also came under further pressure last year from environmental regulations, diminished price advantages of foreign coal over domestic material, and falling coal use. As a result, Chinese coal imports fell 30% y-o-y in 2015 to 188mt. There was still some positivity in the dry bulk sector, as China’s seaborne grain imports grew rapidly by 26% in 2015 to reach 110mt. However, this was not enough to offset the drop in coal imports, and despite growth of 2% in minor bulk imports, China’s total dry bulk imports fell 2% in 2015 to 1,516mt.

Meanwhile, Chinese seaborne imports of crude oil increased 9% y-o-y in 2015 to total 306mt, a similar pace of growth to average expansion seen in 2001-14. Last year, imports were supported by filling of the Strategic Petroleum Reserve, refinery capacity expansion and the initial relaxation of crude import restrictions for some ‘teapot’ refiners. Meanwhile, total gas imports grew by 18% in 2015, on the back of a surge in LPG imports to 12mt.

However, whilst there have been some pockets of positivity for Chinese imports, weak demand for dry bulk cargoes (which account for over 70% of imports) has soured the overall picture. The outlook remains challenging, as iron ore and coal imports may fall in 2016, and the state is aiming to reduce overcapacity in a number of industries. While China is expected to remain a key driver of growth in many trades going forwards, with a maturing economy it seems unlikely that the country can continue to be as strong a driver of overall expansion in global seaborne trade as it has been in recent years.

(Source : Clarkson Research Services Limited)