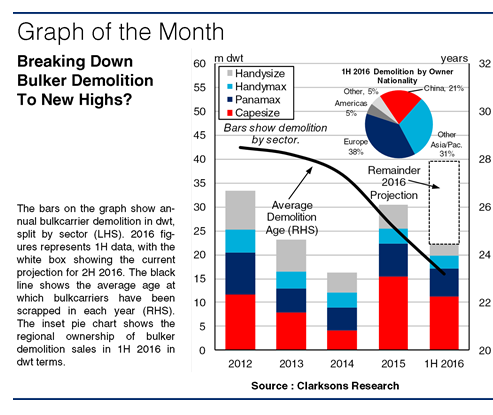

Depressed bulkcarrier market conditions have continued to exert severe financial pressure on owners, with bulker earnings averaging a record low of $4,824/day in 1H 2016. This has led to a firm pace of scrapping so far in 2016, and while demolition activity has slowed somewhat in recent months, the current annual bulker demolition record of 33.4m dwt, set in 2012, seems likely to be challenged this year.

In 1H 2016, 292 bulkcarriers of 22.1m dwt were scrapped, representing a half-yearly record, after 429 ships of 30.5m dwt were recycled in full year 2015. Bulker demolition has also accounted for 77% of all tonnage demolished globally so far this year, up from less than 50% in 2014-15. Meanwhile, the average age at which bulkers have been scrapped has continued to decline, reaching 23 years in 1H 2016, down from 25 years in 2015, and over 28 years in 2012. Now that the half-way mark in 2016 has been passed, what other trends in bulker demolition have been apparent this year?

Scrapping of large bulkers has been an evident feature. In 1H 2016, 66 Capesizes of 11.3m dwt and 80 Panamaxes of 5.7m dwt were scrapped, with Capesize and Panamax demolition together accounting for a significant 77% of total bulker tonnage scrapped. In 2012, demolition was comparatively more balanced between the sectors, and scrapping in the smaller sizes appears to have slowed slightly since then. In 1H 2016, 146 ships of 5.1m dwt in the Handymax and Handysize sectors were scrapped.

Various trends in ownership of units sold for demolition have also emerged. Chinese owners have accounted for the largest share (21%) of bulker tonnage scrapped this year, selling 4.7m dwt. This is in line with Chinese owners’ share of the ‘elderly’ bulker fleet (ships aged over 20 years) at the start of 2016. European owners accounted for 38% of tonnage scrapped in 1H 2016, far exceeding their 23% start year share of the ‘elderly’ fleet, with 50 ships of 3.5m dwt sold by Greek owners alone. In contrast, owners in the Americas appeared more cautious, accounting for 5% of demolition in 1H 2016, compared to their 13% share of the ‘elderly’ bulker fleet.

Meanwhile, recent months have seen a slower pace of demolition activity. In Q1, 175 ships of 14.1m dwt were scrapped, falling to 117 ships of 8.0m dwt in Q2 (sales in June totalled only 1.5m dwt). However, weak earnings and a challenging demand outlook suggests that bulker scrapping may well remain firm in 2H 2016. Assuming that activity picks up in the short-term, demolition in full year 2016 could reach a record 39.5m dwt.

So, while challenging demand trends appear to have limited the impact of firm demolition on the market balance so far this year, supply growth has been successfully limited to less than 1% so far this year. While 2016 will not be remembered as a year in which many highs were reached in the bulkcarrier sector, demolition at least could be one area where a new record level is being set.

(Source : Clarksons)