‘Non-delivery’ of vessels on the orderbook has been a prominent theme in shipbuilding in the last decade, and looks set to be increasing again this year amid troubled shipping markets. Risks to the delivery of the orderbook can emerge from both owners and shipyards, and fluctuations in market conditions can often have a great influence on ‘non-delivery’ trends too.

During shipping market downturns, changes in contracting or demolition often draw the most attention, but deliveries are also an important factor. ‘Non-delivery’ (when vessels on order are delayed or cancelled) can act as another supply-side ‘lever’ to limit the flow of tonnage into the fleet when markets conditions are poor.

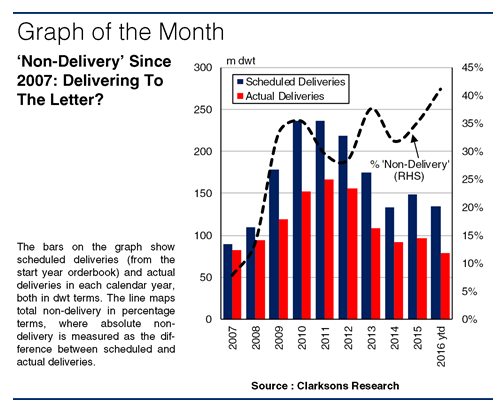

This concept is difficult to measure, but one method is to take the difference between scheduled deliveries from the start year orderbook and actual deliveries. Total non-delivery increased significantly with the onset of the financial crisis, from 8% in dwt terms in 2007 to 33% in 2009. In the year to date this figure has reached 41%, and 2016 seems likely to set a new record.

Non-delivery can be driven by a number of risks to the orderbook. ‘Market risk’ is created by weak vessel demand: in depressed markets there is a greater incentive to delay vessels and non-delivery tends to rise. ‘Owner risk’ emerges when shipowners are unable to make payments or access finance, or if they look to delay the delivery of ships. Finally, ‘yard risk’ is generated by shipyards failing to deliver vessels on time, sometimes as a result of financial problems. Of course, these risks are interlinked, but they provide a framework for analysing non-delivery trends.

In general, the uptick in non-delivery over the past two years has been driven by an increase in market risk across the major sectors. In the bulkcarrier sector weak earnings have persisted through 2016, causing non-delivery to rise to 50% in dwt terms in the year to date, up from 42% in 2015. Although tanker non-delivery has fallen from 32% last year to 23% in 2016 so far, due in part to firm earnings in the first half of the year, the biggest change has been in the boxship sector, where non-delivery has risen from 13% in 2015 to 39%, following a sharp decline in rates across most ship sizes.

Weak markets have also added to owner risk, with many owners negotiating delays to the delivery of vessels, particularly bulkcarriers. This risk has been compounded by the generous payment terms that many owners received, with low upfront costs giving them more power to push back delivery. Yard risk is also a significant factor. Although most builders that have ceased operations have been small, a few larger yards have also left the business, and there are a number of large shipyards in China and Korea that face ongoing financial difficulties.

Overall then, there are a range of risks to the orderbook that can impact whether vessels are delivered on schedule. In the year to date, changes to the market environment have been important across all of the major sectors, and this increased market risk looks set to drive non-delivery to record levels in full year 2016.

(Source : Clarksons Research)