Newbuilding prices have fallen fairly consistently since the end of 2014, and this trend has continued in recent months. Cutting newbuild prices can be an effective way for yards to stimulate new orders, but this is not always the case. A range of factors have dampened the impact of falling prices in 2016 so far, whilst other constraints may have limited the extent of the cuts seen.

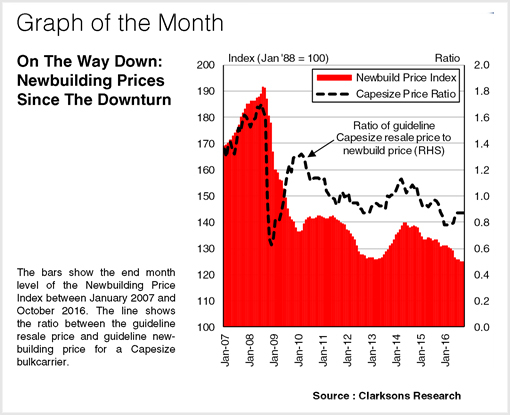

In recent times, the combination of weak demand for newbuildings and excess shipyard capacity have caused newbuild prices (assessed here in nominal terms) to fall to levels not seen since around 2004. Although the scarcity of orders makes it more difficult to accurately gauge price levels, there has been a clear downward trend this year in the Newbuilding Price Index, which has fallen from 131 points at the start of the year to 124 points as of the end of October.

The most significant decreases in newbuild prices in 2016 so far have been in the tanker and containership sectors, where contracting has dropped off sharply since the end of 2015. The guide prices for a c.320,000 dwt VLCC and c.8,800 TEU boxship have fallen 9% and 7% respectively since then. The decline in bulkcarrier prices has been less severe this year, but they have been on a downward trend for a longer period, and the guide price for a c.180,000 dwt Capesize has fallen by 22% since the end of 2014.

Price cuts can be one way for yards to attract orders. However they have had little impact in 2016 so far, with extremely weak markets and demand for new vessels, and limited availability of finance. Moreover, market conditions have led to resale prices offering a potentially more attractive alternative to newbuilding. This has been most notable in the bulker sector, with the guideline resale price for a Capesize falling to 78% of the newbuild price in Q1 2016 (see graph). Resale prices have also fallen to less than 90% of newbuild prices in some boxship sizes.

The potential ability to impact ordering through newbuild pricing can also be limited by constraints on shipyards: it is often difficult for yards to keep cutting prices, especially when they are under financial pressure. Prices at Chinese yards are already below those elsewhere for many vessel types. In South Korea, opportunities for yards to reduce prices may have been constrained by the influence of creditors.

Finally in Japan, some yards with full orderbooks until 2019 or 2020 have likely felt a little less pressure to lower prices, but others may have seen their flexibility limited by the rising yen, which has appreciated by around 15% against the dollar since the start of the year. As a result, prices might not have been cut as sharply as some may have expected, limiting the possible impact on ordering.

So, the impact of dropping newbuild prices has been limited by a range of factors, whilst financial pressures at shipyards have also had an impact on the extent to which prices might be cut. Despite newbuild prices falling further in 2016 so far, it is fairly clear that wider improvements to the market environment will be required to stimulate a fresh wave of vessel ordering activity.

(Source : Clarkson Research)