Developments in global refinery capacity and throughput have a major influence in driving tanker trading patterns and market conditions. In the last few years the expansion of capacity in the Middle East and Asia have been headline stories. However, since the decline in the oil price, the refinery sector has seen significant changes in dynamics and this year a number of key trends have become apparent.

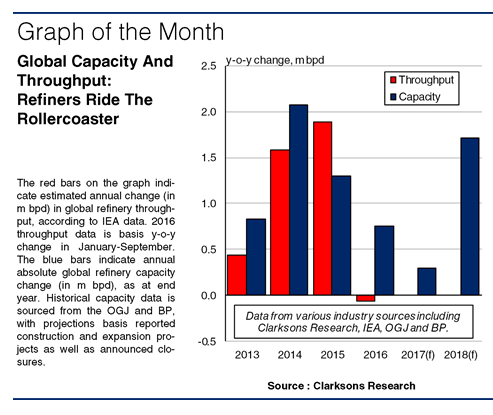

The first of these trends has been a slowdown in refinery capacity growth. Between start 2014 and end 2015 global refinery capacity expanded by 3.4m bpd to 98.1m bpd, on the back of newly constructed refineries in the Middle East and Asia. In the Middle East, plants such as the 0.4m bpd Yasref facility were aimed at exporting products overseas, whilst the expansion of capacity in China (which accounted for c. 30% of global growth in 2014-15) was generally aimed at the domestic market.

However, global capacity expansion is slowing, with growth of 0.8m bpd projected this year and just 0.3m bpd in 2017. This largely reflects fewer Middle Eastern, Chinese and Indian refinery projects. In addition, closures in areas such as Japan and Europe have continued, including the 0.16m bpd La Mede plant in France, which is scheduled to cease refining crude at the end of this year.

Secondly, there has been a lack of global throughput growth this year. In 2014 and 2015 global throughput rose by an estimated 1.6m bpd and 1.9m bpd respectively. Initially this was supported by the ramp-up of activity in newly completed plants. However, following the decline of the oil price from Q3 2014, refinery margins in several countries improved. This supported a surge in throughput in many regions, with throughput in OECD Europe up 6% in 2015 to 12.1m bpd.

But global throughput growth has not continued into this year, having fallen slightly y-o-y in the first nine months of 2016. This is largely due to high product stockpiles in many regions depressing margins. Additionally, strikes in France during the summer, the closure of 0.1m bpd of capacity at the Lindsey plant in the UK and continued disruptions in South America have all held back throughput levels.

Thirdly, while throughput has fallen on a global level, one important element of growth has been Chinese ‘teapot’ refineries, following the recent liberalisation of the Chinese crude import market. The impact of this can been seen in the 19% y-o-y growth in refinery throughput in Shandong, where a significant proportion of ‘teapot’ refiners are located. This compares to an increase of 3% y-o-y in total Chinese refinery throughput, and has led to significant changes in the refinery sector in China and elsewhere in Asia.

So, although there have been some areas of growth, global throughput appears unlikely to rise firmly in 2016. Looking to next year, expectations for continued limited growth in refinery capacity and throughput are a key factor in the projected slower rate of seaborne oil trade growth. Although these are uncertain times for the oil sector as a whole, trends in the tanker market will still be closely tied to the ongoing ups and downs of the global refinery sector.

(Source : Clarkson Research)