In 2016, market conditions across most sectors of the shipping industry have been highly challenging. The ClarkSea Index, which illustrates the fortunes of earnings for the major commercial ship types makes fairly clear the fate of the volume shipping sectors, but how is the wider global fleet covered by World Fleet Monitor faring now, in comparison to the post-downturn period as a whole?

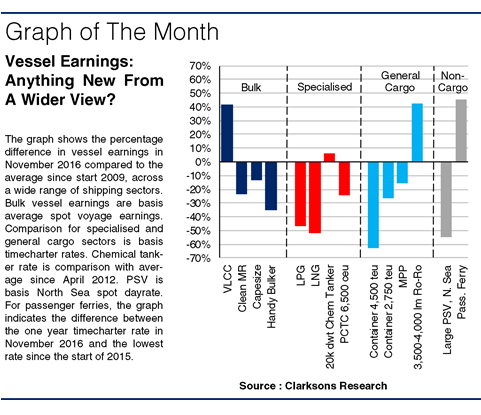

The ClarkSea Index, an average of earnings for tankers, bulkers, boxships and gas carriers, averaged $10,574/day in November 2016, down 11% on the average since the start of 2009, a handy marker for the onset of the downturn. In the dry bulk sector, the market has been under significant pressure for some time, and in November 2016, Capesize spot earnings stood 14% below the average since 2009.

Meanwhile, oil tanker earnings have fallen this year, from a strong 2015, despite robust trade growth. Firm fleet growth in both the crude and product tanker sectors has placed pressure on the tanker markets, with clean MR average spot earnings in November 23% below the average since start 2009. To see how the wider shipping fleet is faring, the graph shows the same comparison for a broad range of sectors.

")

Clearly, the specialised shipping sectors are faring little better. LPG market conditions have deteriorated acutely this year, reflecting the impact of rapid fleet growth, taking the one year VLGC timecharter rate from over $70,000/day in mid-2015 to just $17,466/day in November 2016. LNG market conditions have remained challenging, but may have now bottomed out.

The PCTC market has also come under pressure, with the rate for a 6,500 ceu vessel averaging $16,000/day in November, down 24% on the average since start 2009. In the general cargo sector, the boxship charter market has been notably depressed, with rates at bottom of the cycle levels. The 6-12 month charter rate for a 2,750 TEU boxship stood at $6,050/day in November, 26% lower than the average since start 2009.

However, in some of the niche general cargo areas, things look a little better; timecharter rates for Ro-Ro vessels have firmed this year, with the rate for a 4,000 lm vessel standing at €18,000/day in November, up 43% on the average since 2009. Into the ‘non-cargo’ sectors, conditions in the offshore sector remain under extreme stress as the industry grapples with low oil prices and cuts in E&P budgets.

")

The North Sea spot day rate for a large PSV fell to £4,994/day in November, 55% below the average since the start of 2009. But again some niches are performing more strongly, with passenger ferry charter rates in November up 46% on their start 2015 level, and the cruise sector in full-on expansion mode.

In general, comparing today to the downturn period as a whole, things in many sectors appear to be as bad as they have ever been. In the wider fleet some niche sectors have seen better earnings, but even so, most shipowners will surely be hoping that 2017 brings with it a significant change in fortunes.

(Source: Clarkson Research Services)")