After a long cycle of build-up in capacity in the 2000s, shipyards hit a new peak in global output in 2010. Since then, the impact of reduced vessel ordering on shipbuilders worldwide has been a key issue for the industry, and it’s clear that global output has dropped significantly and shipyard capacity has diminished. But how far can those shipyards still active look ahead today?

‘Forward cover’ is one basic indicator of the volume of work that shipyards have on order, calculated by dividing the total orderbook by the last year’s output (in CGT). Unsurprisingly, after a period of extremely low ordering in 2016, forward cover has shortened.

Currently, global forward cover stands at 2.3 years having declined throughout 2016, as the orderbook shrank by 25% in CGT terms. Global forward cover was as low as 2.1 years at the start of 2013 (but delivery volumes in 2012 were 37% higher than in 2016) and peaked at 5.6 years in 2008.

")

Looking around the shipbuilding world, yards in Korea currently have the lowest level of cover at 1.5 years. European yards, meanwhile, bucked the trend in 2016, increasing their forward cover on the back of cruise ship orders (and falling production volumes) to 4.2 years.

Fewer fresh orders have also led to a greater number of yards ending the year without receiving a single contract. During 2005-08, the number of yards to take at least one order was on average equivalent to 87% of the number of yards active (with at least one unit on order) at the start of the year.

In 2009-15, with ordering generally lower, the figure averaged 49%. In 2016 this fell further to 28%, with just 133 yards receiving an order. In China, 48 yards (26 of which were state-backed) won an order in 2016 compared to 284 yards in 2007. In Japan, 22 yards took an order in 2016 compared to 60 as recently as 2015. In Korea, 11 shipyards took an order last year.

")

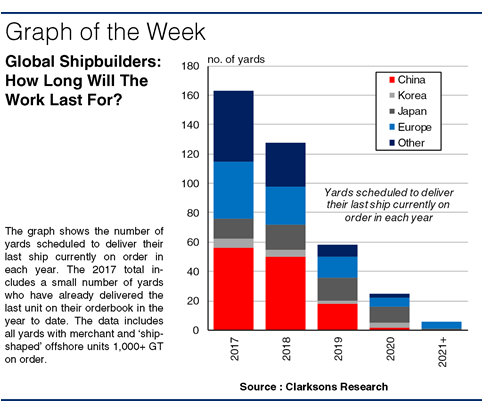

Whilst many yards have tried to cope with the lower demand environment by slowing production or working outside their traditional product range, the statistics clearly point to huge challenges. In 2016, 117 yards delivered the final unit on their orderbook. The peak production level of these yards, many of them smaller builders, totals around 4m CGT. However, 163 yards are scheduled to deliver their current orderbook by the end of 2017 (although in reality slippage may mean some of the work runs on past the end of the year).

Statistically, this represents 43% of the number of yards active at the start of the year. Although these yards have been reining back capacity and outputting less in recent years, the peak production level of this set of yards totals as much as 12m CGT. Offshore builders of course face huge pressures too, with about half of those active scheduled to deliver their final unit on order this year.

Global shipyard output and capacity have fallen significantly since the peak years. However, many remaining yards still don’t need to look too far ahead to see the end of their current workload. The shipbuilding industry will be hoping to see a return to a more active newbuilding market sooner rather than later.

(Source : Clarksons)")