The US is the second largest importer of crude, but also the biggest oil producer globally. Recently, there have been a number of changes in US oil dynamics which could have a significant impact on seaborne crude trade. However, there is considerable uncertainty over the trajectory of US crude volumes this year given the many different factors at play. What are the most important drivers to consider?

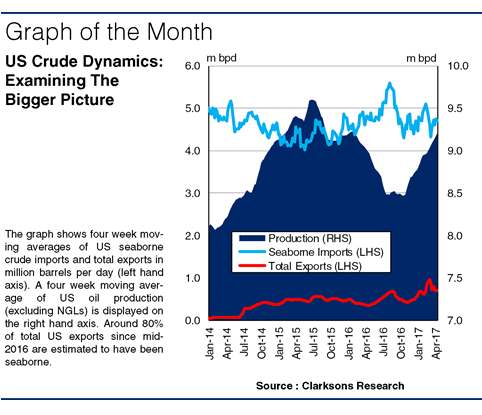

One key driver of changes in US crude imports is US oil production. Following the US ‘shale revolution’, 2014 saw the US become the world’s top oil producer, with output peaking at 9.6m bpd in mid-2015. However, the subsequent oil price collapse exerted pressure on shale producers, and US oil output dropped to 8.4m bpd in 2H 2016. Overall, US oil production declined by 0.40m bpd in 2016, supporting a 0.45m bpd (10%) increase in US seaborne crude imports to 4.64m bpd.

But, with domestic output rising again since late 2016 in line with an improved oil price, there are potentially negative implications for crude imports. However, there remain a range of scenarios for the oil price this year, and given the sensitivity of US producers to oil price levels, the outlook for US oil output and crude imports remain subject to uncertainty.

")

Adding an extra dimension to the current dynamics are US crude exports. The US lifted its crude export ban at the end of 2015 after 40 years, although due to the saturated international oil market and falling domestic production, US exports initially remained limited. However, since early 2017, exports have risen notably, hitting a record 1.2m bpd in February, with reports of increased shipments on long-haul routes to Asia.

This has reflected the recent revival of output, improved US export infrastructure and some buyers seeking to diversify supply. Rising exports have contributed to the uncertainty over US crude imports this year, as many US refineries are geared for heavy grades of crude. If exports can provide an outlet for surplus light oil production, imports of heavy oil may not be as significantly affected by increasing output.

Meanwhile, US crude inventories have also made headlines lately, with stocks reaching record highs of over 1.2bn bbls in February. However, in early April, stocks were drawn down for two consecutive weeks. If refineries continue to draw upon US inventories, this could potentially dent crude imports.

")

Yet another variable is the potential fluctuations in landborne trade between the US and Canada, which could displace seaborne imports. Finally, pipeline developments such as Dakota Access and much further ahead Keystone XL, could better facilitate US refiners’ access to crude, which could also undermine US seaborne imports.

So, while the current projection is for US crude imports to soften this year, there remains uncertainty given the many factors involved. Rising US crude exports could also drive interesting changes in crude trade patterns. Thus, it remains to be seen precisely how US crude trade will develop, but the outcome either way will still be significant for the crude tanker market.

(Source : Clarksons)")