")

China’s rapid economic growth over the last two decades has seen the country’s annual primary energy demand more than triple. Coal aside, the other key fuels powering China’s developing economy have been oil and gas. And while commodity imports have risen, economic growth has also incentivised more E&P activity in China itself. So how are things looking for China’s upstream sector, particularly offshore?

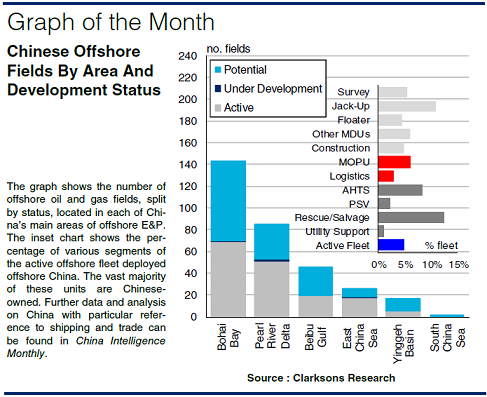

As of start May 2017, a total of 319 fields had been discovered offshore China (with 163 of these having been brought into production at some point) and around 5% of the active offshore fleet (over 500 units) was deployed in the country. Moreover, in 2017, 15% of total projected Chinese oil and gas production (4.43m boed) is forecast to be produced offshore.

Of course, things were not always thus. While oil extraction in China is thought to date back to antiquity, the modern industry took off during the era of Mao Zedong, in the 1950s and 1960s, with the exploitation of fields in the onshore Songliao Basin, notably the Daqing Complex, by the state. Offshore E&P was minimal before the late 1980s.

As was the case in many countries, Chinese offshore oil production began at shallow water fields, in China’s case located in the Bohai Bay, Pearl River Delta and Beibu Gulf areas, which still account for 43%, 32% and 12% of the fields now active off China.

A total of 139 offshore fields are in production across these three areas, of which 76% are exploited via fixed platforms. Shallow water E&P heavily influenced the development of the offshore fleet in the country: for instance, 11% of the active global jack-up fleet is deployed off China.

In recent years though, the drive to raise production has seen Chinese E&P shift into deeper waters, in mature areas as well as frontiers in the East China Sea, the Yinggeh Basin and the South China Sea. That being said, just 13 fields in depths of at least 500m have been found to date (the first in 2006), of which only two are active: Liwan 3-1 and Liuhua 34-2, both in the Pearl River Delta.

")

Hence demand for high-spec floaters, MOPUs and OSVs remains limited. Deepwater E&P in China was led by IOCs, but then CNOOC began concerted independent efforts. However, this process has been slowed by the oil price downturn, which prompted the NOC to put deeper water projects such as Lingshui 17-2/22-1 and Liuhua 11-1 Surround on the backburner.

The outlook for Chinese offshore projects seems to have improved since the OPEC deal though, and CNOOC is reportedly planning over 120 offshore exploration wells in the next five years. But there are contrary factors, not least of which is political risk in the East and South China Seas, where China and neighbours such as Japan and Vietnam are engaged in bitter border disputes, notably over the “nine dash line”. Moreover, government plans to increase onshore shale gas output at Fuling and elsewhere may divert investment from costly offshore projects.

So there are clearly risks to continuing E&P off China in more frontier areas. But even as the country’s economy matures, energy demand growth is likely to remain substantial. The fundamentals thus suggest that the onwards march of E&P off China is likely to be far from over yet.

(Source : Clarksons Research)")